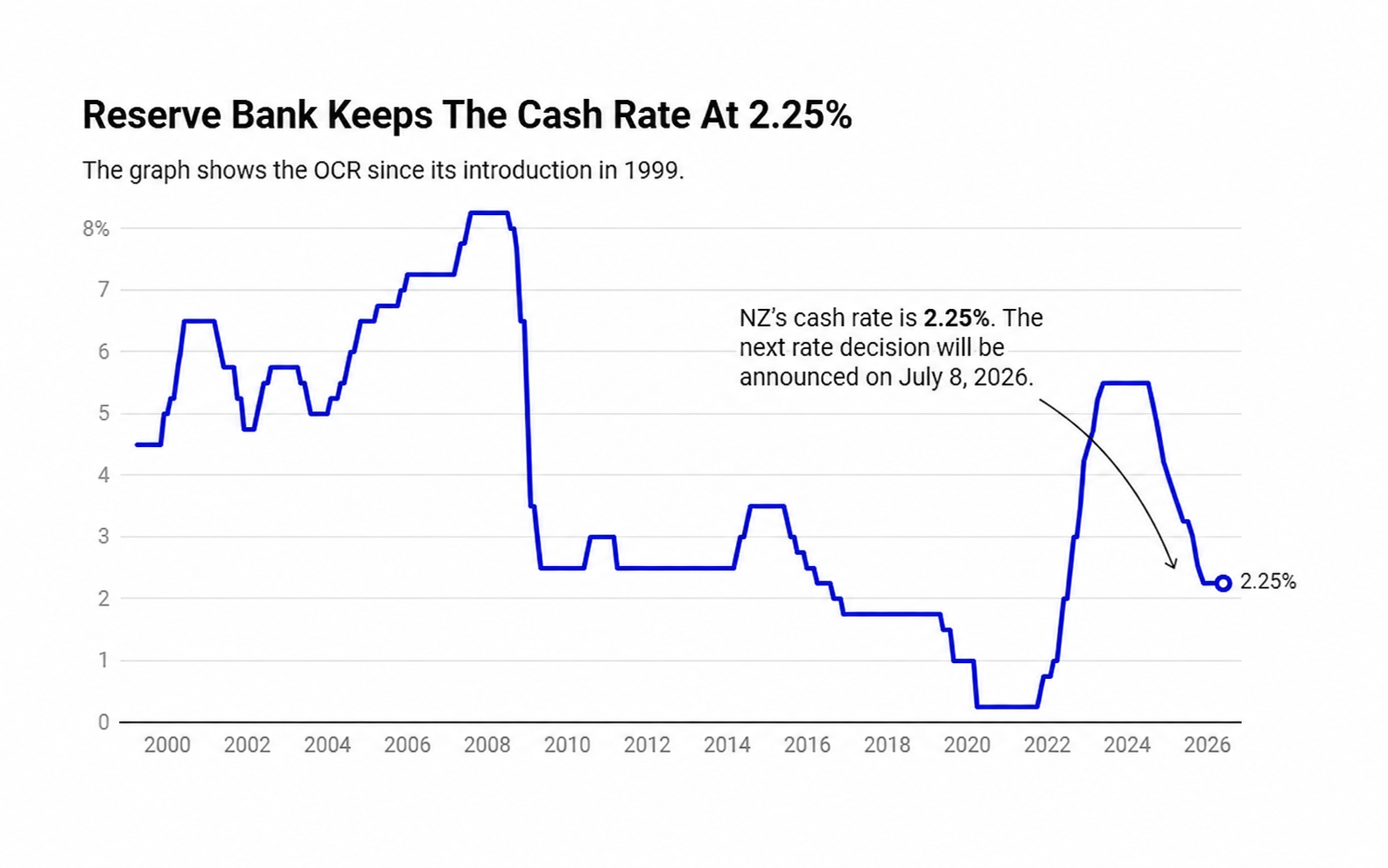

The Reserve Bank’s decision to hold the Official Cash Rate at 2.25% on Wednesday, 27 May may sound like good news for borrowers at first glance, but the message behind the decision is more cautious than comforting.

Source: OneRoof.co.nz

The OCR has not gone up yet. However, the Reserve Bank has made it clear that future increases are now more likely, and potentially sooner than previously expected. The decision was also finely balanced, with three members of the Monetary Policy Committee voting to increase the OCR, before Governor Anna Breman cast the deciding vote to keep it on hold.

For mortgage holders, first-home buyers and property investors, the key takeaway is this: the low point for interest rates may now be behind us.

Why Did the Reserve Bank Hold the OCR?

The Reserve Bank is currently trying to manage two competing problems.

On one hand, inflation remains a concern. Higher global energy prices, driven by ongoing disruption in the Middle East, are feeding through into fuel, transport and other business costs. The Reserve Bank has warned that the OCR may need to increase sooner and by more than previously expected if these cost pressures become embedded in everyday prices and wages.

On the other hand, the New Zealand economy is still fragile. Consumer confidence has fallen, business confidence and spending are weaker, profit margins are under pressure, and the housing market remains soft.

That is why the Reserve Bank held fire for now. Raising rates too quickly could add more pressure to households and businesses. But leaving rates too low for too long could allow inflation to become harder to control.

So while the OCR stayed at 2.25%, this was not a “nothing to see here” decision. It was more of a warning shot.

What This Means for Mortgage Holders

For existing mortgage holders, the biggest risk is not necessarily an immediate jump in repayments today. The bigger issue is what happens when loans come up for refixing over the next 6 to 12 months.

Shorter-term mortgage rates are usually more sensitive to changes in the OCR. If the Reserve Bank does begin lifting the OCR later this year, borrowers on floating rates, short fixed terms, or loans coming up for renewal could feel the impact first.

Longer-term fixed rates may also remain under upward pressure because banks price them partly off wholesale funding markets, which had already started moving higher as markets anticipated a tighter interest-rate path. Reuters reported that after the RBNZ decision, markets were pricing in a higher chance of a July hike and a total of around 72 basis points of tightening across the year.

For homeowners, this is a good time to review the structure of your mortgage rather than assuming rates will fall again soon. That does not automatically mean everyone should rush into the longest fixed term available. It does mean borrowers should think carefully about repayment buffers, refixing dates and whether splitting a loan across different terms could help manage uncertainty.

The most important point is preparation. A borrower who has already stress-tested their repayments has more control than one who waits until their fixed rate expires and reacts under pressure.

What This Means for First-Home Buyers

For first-home buyers, the situation is mixed.

Higher mortgage rates can reduce borrowing capacity and make bank servicing tests more difficult. That can be frustrating, especially for buyers who were hoping interest rates would continue falling through 2026.

But there is another side to the market.

Property prices have stalled, and in some areas, softened. REINZ’s April data showed national median house prices fell 0.5% from March and were 0.6% lower than a year earlier, while national sales were also down year-on-year. Interest.co.nz’s coverage of the same REINZ data described the market as particularly soft heading into winter, with Auckland sales down 29.5% compared with March and the REINZ House Price Index down 1.2% nationally for the month.

Source: Interests.co.nz

For serious buyers, that can create opportunity.

When prices are moving rapidly, buyers often feel pressured to make quick decisions. In a slower market, there is usually more time to compare options, negotiate properly and focus on the long-term suitability of a property rather than simply trying to beat the next buyer.

That does not mean every property is a bargain. Good homes in strong locations still attract attention. But buyers who are finance-ready, realistic and clear on what they want may find themselves in a stronger position than they were during the hotter parts of the market.

What This Means for Property Investors

For investors, the OCR hold reinforces the need to run the numbers conservatively.

A stalled property market can be attractive because it reduces the risk of buying into overheated pricing. Investors may have more room to negotiate, more stock to choose from and less urgency from competing buyers.

However, rising or uncertain interest rates can quickly affect cash flow. That means investors should be looking closely at rental yield, holding costs, insurance, rates, body corporate fees, maintenance and the potential for vacancy.

The best investment decisions in this kind of market are not usually based on trying to pick the exact bottom. They are based on buying well, in a location with long-term fundamentals, at a price that still makes sense if interest rates rise further.

ANZ’s latest Property Focus notes that the housing market is facing headwinds from higher fuel prices, softer growth, possible OCR increases and election-year uncertainty, and it continues to expect house prices to fall slightly over 2026.

In other words, the market is not running away from buyers right now. That gives investors time to be selective.

Is 2026 a Good Time to Buy?

The answer depends on your position.

If your finance is stretched, your income is uncertain, or you are relying on interest rates falling quickly, caution is sensible.

But if you are in a strong financial position, have pre-approval or a clear lending pathway, and are buying for the medium to long term, 2026 may offer a better buying environment than many people realise.

Prices have stalled. Buyer activity is measured. Sellers are generally more realistic than they were during the peak. And while interest rates may rise from here, that risk is already creating some of the very conditions that can make the market more attractive for prepared buyers.

The key is not to buy because of one OCR announcement. The key is to understand the wider market and make a decision based on your goals, your numbers and the quality of the property in front of you.

Watermere Residences: Boutique Homes in Karaka

For buyers looking in South Auckland, Watermere Residences in Karaka is one development attracting increasing attention.

Located at Waimarie Drive, Karaka, Watermere Residences is a boutique collection of just 12 homes, offering a mix of 3 and 4-bedroom layouts, each with double car parking. Three homes have already sold, including both 5-bedroom residences, with a few more currently under negotiation.

We are also seeing demand lift. The viewing calendar is already around 70% booked for this weekend, with more enquiries coming through as buyers take a closer look at the opportunity in the current market.

Open home times this weekend:

Saturday: 1pm – 4pm

Sunday: 12pm – 4pm

Monday to Friday: Anytime, by appointment only

You can meet us at the open home this weekend at 2 Wehi Drive, Karaka. Due to roadworks, please take exit 461 and turn right into Victoria Street.

If you have not booked a time yet, we encourage you to do so. If the open home times do not suit, feel free to contact us directly to arrange a private viewing.